Access to education has never been easier with Student Loan options that are tailored to your individual needs. Unfortunately as of this writing, May 2023, interest rates are at an all-time high. High-interest rates are often scary when you look at a total payoff amount that is much higher than your total loan amount. (If that scares you look at a 30 year ammitorization table on a home mortgage – yikes)

Student loan debt is a challenging financial hurdle faced by millions of young professionals across the globe. If you are one of them, you are probably thinking two things right now

1. I cannot afford this right now I need to think of another option

2. How can I pay this off quicker

With careful planning and disciplined budgeting, it’s entirely possible to accelerate your debt repayment and save money on interest. Fortunately with Coding Temples placement rate and high salaries – this is an investment that pays off.

Let’s explore a practical approach to repaying a $15,000 student loan on an $80,000 annual salary.

Know Your Loan

Before creating a repayment plan, it’s crucial to understand your loan’s specifics. If you borrowed $20,000 at an APR of 5%, the total amount you owe will grow each year if you only make minimum payments. The faster you pay off the loan, the less you’ll pay in interest over time.

Your Salary, Taxes and Net Income

An $80,000 salary is a substantial income, but remember that not all of that money lands in your pocket. You have to account for taxes and other deductions. For simplicity, we’ll use a rough estimate and say that after federal, state, and local taxes, you’ll take home about $60,000, or $5,000 per month.

Constructing a Budget

Creating a budget is a critical step. A good rule of thumb is the 50/30/20 budgeting principle: 50% of your net income goes to needs, 30% to wants, and 20% to savings and debt repayment.

- Needs (50%): These are your essential living expenses, such as housing, utilities, groceries, healthcare, and minimum loan payments. On a $5,000 monthly net income, this would amount to $2,500.

- Wants (30%): These are non-essential expenses, including entertainment, dining out, hobbies, etc. This would amount to $1,500 per month.

- Savings & Debt Repayment (20%): This is where your extra loan payments will come from. This amounts to $1,000 per month.

Accelerating Loan Repayment

With your budget in place, let’s allocate half of your savings and debt repayment portion ($500) to your student loan each month. This is on top of your minimum monthly payment.

Using a student loan repayment calculator, if you paid $500 extra per month towards your $15,000 loan with a 6% APR, you could pay off your loan in less than two years instead of 6, save over $2,500 in interest and 50 months of time!

*These numbers illustrate the significant impact that additional payments can have on the total cost and duration of a loan. However, it’s always important to make sure any plan to pay off a loan early fits within your broader financial strategy and budget.”

Other Strategies to Consider

- Decrease your expenses: If there’s room to cut back in your “wants” category, that extra money could be used to pay off your loan faster.

- Employer assistance programs: Some employers offer student loan assistance. If your employer does, take advantage of it!

- Refinancing your loan: If you have a solid credit score, you could refinance your loan for a lower interest rate. This could save you money over the lifetime of your loan.

In conclusion, repaying a student loan faster involves a combination of careful budgeting, discipline, and strategic financial planning. By making extra payments, increasing income, decreasing expenses, and considering refinancing, you can pay off your student loan quicker and save money on interest. Remember, everyone’s situation is unique, and it’s important to tailor your approach to your individual circumstances.

To calculate monthly money saved on interest when paying off a loan early, we would first need to determine the total interest paid over the life of the loan if only minimum payments were made, compared to the total interest paid when making additional payments. The difference between these two figures, divided by the number of months in the loan term, would give the monthly interest savings.

Here’s an illustrative example of how early payments might impact your student loan over the course of 5 years (72 months). In this example, we’ll assume a minimum payment of $255 per month (which would typically pay off a $15,000 loan at 6% APR over 5 years), compared to a payment of $457 per month (which would pay off the same loan in about 3 years). The numbers might not be precise due to compounding and how interest is calculated, but they should give you a general idea.

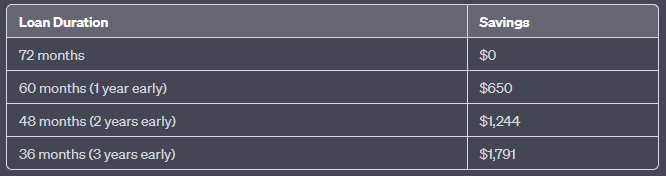

To pay off a loan faster, you’ll need to make larger monthly payments. The following table shows the standard monthly payment for a $15,000 loan at a 6% interest rate paid off over 72 months, and then what the monthly payments would be to pay off the loan in 60 months (1 year earlier), 48 months (2 years earlier), and 36 months (3 years earlier).

Keep in mind these figures are approximations, and actual numbers might slightly differ due to daily compounding of interest and how payments are applied. For exact figures, you may wish to use a detailed amortization calculator or consult with a financial advisor.

For simplicity, we will not take into account the effect of taxes on the $80,000 salary in this example. Here’s the breakdown:

Now, to see the savings when you pay off the loan faster, you can subtract the total paid in the early repayment scenarios from the total paid if you took the full 72 months to pay off the loan. Here’s how much you’d save:

These savings come from the reduced amount of interest you pay over the life of the loan when you pay it off early. Remember, though, that increasing your monthly payment can put more strain on your monthly budget, so it’s important to make sure any plan to pay off a loan early fits within your overall financial plan.

Explore your Financing Options

To learn more about our financing options and how you can be well on your way to a technical role earning up to six figures, speak with an Admissions Specialist at Coding Temple.